TELANGANA BUDGET 2026- SOCIAL ECONOMIC OUTLOOK

21-03-2026 12:00:00 AM

Telangana's Public Finances: Navigating Sustainability amid Growth Imperatives

Public finance forms a foundational element of any state's development architecture, shaping economic stability, the quality of public service delivery, and the ability to address pressing social and developmental needs. In Telangana, the challenge lies in achieving long-term fiscal sustainability while responding to evolving socio-economic demands. Since its formation, the state has grappled with structural fiscal issues, but recent years have seen a deliberate shift toward greater discipline and transparency.

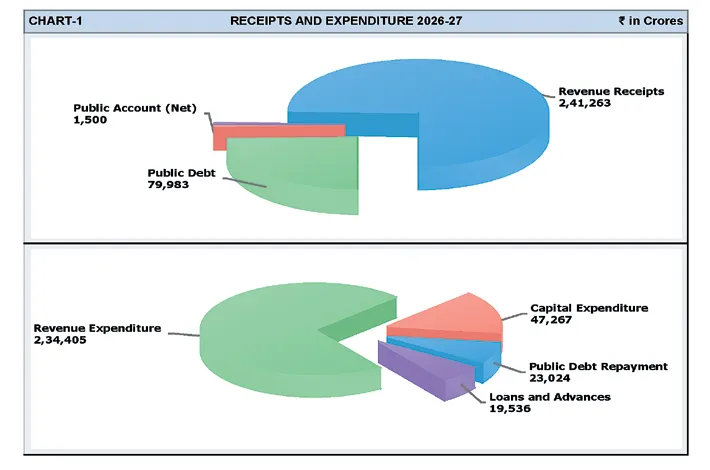

The 2025–26 Budget embodies this strategy, targeting consolidation while advancing development. It focuses on efficient spending, revenue enhancement, legacy issue resolution, and sustained core services. Budget Estimates for 2025–26 show total receipts at Rs 3,04,367 crore, with revenue receipts at Rs 2,29,721 crore and capital receipts at Rs 74,646 crore—indicating stronger mobilization than the previous year's revised estimates.

Revenue receipts break down as state own tax revenue Rs 1,45,420 crore (63.3%), non-tax revenue Rs 31,619 crore (13.8%), central taxes share Rs 29,900 crore (13.0%), and grants-in-aid Rs 22,783 crore (9.9%). Own taxes dominate, highlighting self-reliance efforts. Total expenditure reaches Rs 3,04,865 crore, led by revenue expenditure at Rs 2,26,982 crore (recurring costs) and capital expenditure at Rs 36,504 crore (infrastructure). Additional components include loans and advances (Rs 21,351 crore) and capital disbursements/public debt repayment (Rs 20,028 crore).

Within revenue expenditure, development spending totals Rs 1,79,102 crore (78.9%), split into social services (Rs 1,10,967 crore, up sharply from Rs 58,610 crore in 2023–24) and economic services (Rs 67,722 crore, from Rs 54,258 crore). This expansion emphasizes welfare, education, health, agriculture, and infrastructure. Debt servicing features prominently, with interest payments on FRBM loans at Rs 19,369 crore—a legacy burden pressuring the budget, as such costs do not reduce principal. Public debt receipts under FRBM areRs 69,539 crore (mainly market borrowings and central loans), with repayments at Rs 20,028 crore, showing borrowings partly fund repayments.

State GST led (34.9% share), rising to Rs32,165 crore; sales tax (27.3%) to Rs25,127 crore; excise (19.0%) surged to Rs17,506 crore (strong Q3); stamps/registration (12.3%) to Rs11,304 crore; motor vehicle tax (5.7%) stable at ~Rs5,288 crore. Quarterly trends reflect steady growth, especially in excise and SGST.

The budget projects a revenue surplus of Rs 2,738 crore, covering routine needs including interest. Fiscal deficit stands at Rs 54,010 crore, financing capital investments—deemed more sustainable than revenue spending borrowings. Fiscal performance through December 2025 shows progress in own tax revenue April–December collections rose from Rs 86,152 crore (2024–25) to Rs 92,197 crore (2025–26), broad-based across heads. Comparative profile (2023–24 audited data) places Telangana's revenue receipts at 11.6% of GSDP—moderate versus high-transfer states (Bihar 22.7%, Odisha 20.8%) but stronger than peers like Maharashtra (10.6%) or Karnataka (9.1%).

Development expenditure (revenue + capital) is 11.1% of GSDP, mid-range among general category states—below Chhattisgarh (19.9%) or Bihar (19.3%) but above Maharashtra (8.5%) or Kerala (6.3%).Interest payments (FRBM loans) absorb 14.4% of revenue receipts—mid-tier, lower than Punjab (25.3%) or Kerala (21.7%), but higher effective burden including off-budget items.Debt dynamics (Dec 2023–Dec 2025) show fresh borrowings of Rs3,19,179 crore nearly offset by repayments (Rs3,04,202 crore: principal Rs1,90,131 crore + interest Rs1,14,071 crore). Outstanding debt rose to Rs8,00,805 crore, driven by legacy interest, principal repayments, and welfare/development needs—emphasizing credibility despite pressures.

The Sixteenth Finance Commission (2026–31) retains vertical devolution at 41%. Horizontal formula introduces GDP contribution (10% weight), with Telangana's share rising to 2.174% (from 2.102%). Local body grants and disaster funds support decentralized efforts. The Commission urges 3% GSDP fiscal deficit cap, no off-budget borrowings, and full liability disclosure for sustainability. Telangana's fiscal path reflects consolidation amid welfare priorities. Sustained revenue growth, expenditure rationalization, and prudent debt management—prioritizing productive capital—will enhance capacity, flexibility, and inclusive progress.